Since interest rates have jumped and home prices have come down, I’ve been having weighty discussions with both sellers and buyers. Many sellers are also hoping to buy, and there’s a lot of fear out there I’d like to help dispel. Read on for some insight relating to the things we’ve been talking about.

The way I see it, right now is a better time to buy, compared with when interest rates were lower. There’s opportunity to take advantage of the market situation and be better off financially.

Here’s why and how.

Scenario 1 — $750,000 vs. $600,000

Let’s say you bought a property earlier in the year when prices were higher (largely due to low rates).

At $750,000 with a 5% interest rate and 10% down on a 30-year fixed mortgage, monthly payments would be $3,624 and a $75,000 down payment.

Higher rates are bringing lower prices, with some homes down 20% from their peak*. At a purchase price of $600,000 with a 7% interest rate and 10% down, monthly payments would be $3,593 and a $65,000 down payment.

This equates to $31 less per month and $10,000 less cash for down payment. On top of that, by negotiating a seller credit at closing one can potentially reduce their rate by .25% to 1%, depending on the discount points and credit amount negotiated. This widens the delta even more, potentially reducing payment by an additional $200 to $400 each month.

Let’s look at a higher price point to further demonstrate this.

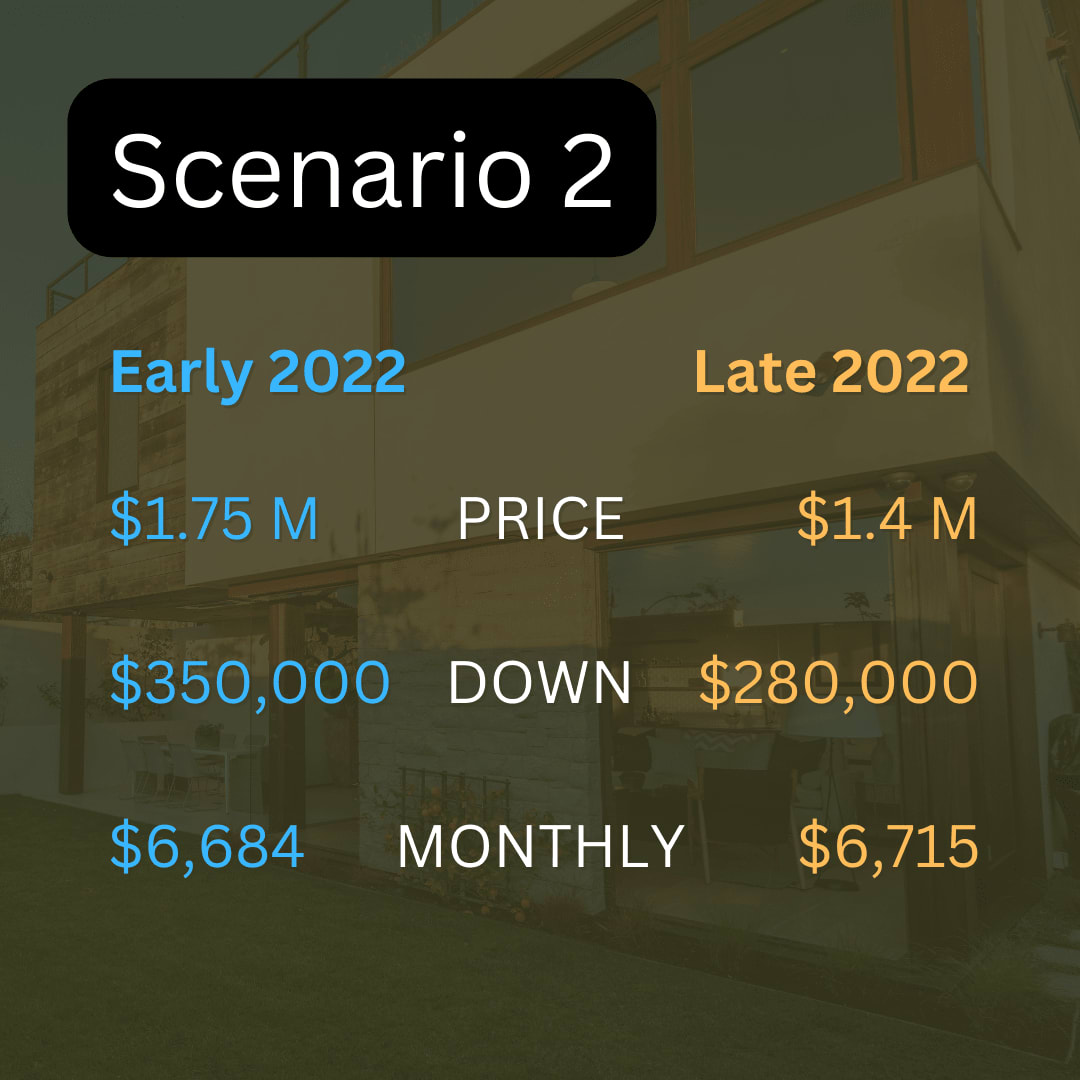

Scenario 2 — $1,750,000 vs. $1,400,000

There are homes selling for $1.4 million today that would likely have sold for over $1.7 million at the peak of the market.

Payment on a 30-year fixed mortgage with 20% down on a $1,750,000 price at a 4% rate is $6,684 per month whereas a $1,400,000 price at a 6% rate is $6,715 per month.

That’s arguably the same cost per month! And a $70,000 down payment savings! Adding in a reduction of payment via a seller credit brings payment down significantly.

Buy now or wait?

Once interest rates start to decrease consistently (which experts suggest will be sometime next year) demand and prices will quickly start to trend upward. This uptick will make the monthly net cost near where it is currently — potentially even higher, since buying down the rate will be less possible. When demand starts to surge again, it will happen quickly, and price escalations will likely follow.

Additional advantages for current buyers include a greater selection of homes, less competition, and more time to consider a property and conduct due diligence (inspection). Compared to where the market has been, there are real advantages to buying now, and with the right strategy one can benefit substantially in the long term.

For those still reading, another strategic way to take advantage of the market is to secure a five-year adjustable-rate mortgage (ARM) loan, which typically has lower rates. Then, when rates come down by about 1%, refinance into a 30-year fixed mortgage. Using this strategy, one can secure a lower price and start paying down the principal on their loan.

Because everyone’s situation is unique, it’s critical to consider all aspects carefully. My team and I take pride in taking a holistic approach to supporting our clients. We know you have a lot to consider when buying or selling your home, and we’re here to help.

- Phillip Belenky

* Price differences do not reflect market averages. Scenarios are hypothetical and used to demonstrate the types of opportunities that can be found in today's market.